Risk Management Toolbox provides functions and interactive workflows for mathematical modeling and simulation of credit, insurance, and market risk. You can perform lifetime credit modeling of probabilities of default (PD), exposure at default (EAD), and loss given default (LGD), as well as expected credit loss (ECL) calculations. You can assess corporate and consumer credit risk, create credit scorecards, estimate probabilities of default, perform credit portfolio analysis, and backtest models to assess potential for financial loss. The toolbox lets you identify important scorecard variables using the predictor screening tools and use the Binning Explorer app to automatically or manually bin variables for credit scorecards. It also includes mortality and unpaid claims models to quantify and analyze insurance risk. Market risk can be assessed with backtesting and simulation tools to evaluate value-at-risk (VaR) and expected shortfall (ES).

Create and analyze credit scorecards, perform predictor screening, explore fairness metrics, conduct stress tests, and model probabilities of default (PD).

Corporate Credit Risk Modeling

Analyze corporate default probabilities, simulate credit portfolio value changes due to credit rating migrations and defaults, identify concentration risks, and calculate regulatory capital requirements.

Backtesting Models for Market Risk

Assess the accuracy of value-at-risk (VaR) and expected shortfall (ES) models by evaluating their predictive performance and comparing them with actual outcomes.

Lifetime Models for Probability of Default (PD)

Estimate the probability of default (PD) based on lifetime analysis with macroeconomic scenarios using MATLAB. PD models include Logistic, Probit, and Cox models.

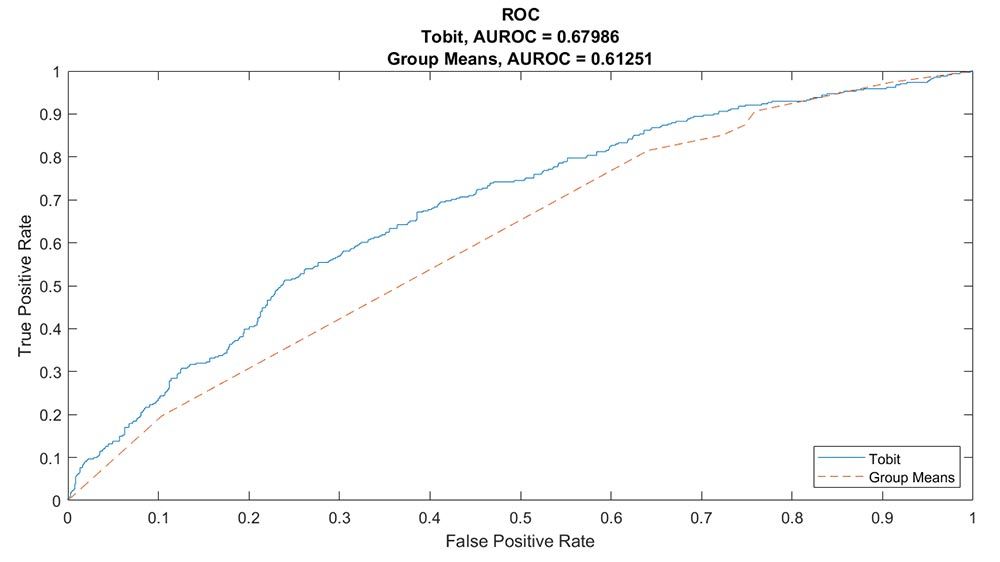

Loss Given Default (LGD) Models

Estimate loss reserves using regression and Tobit models.

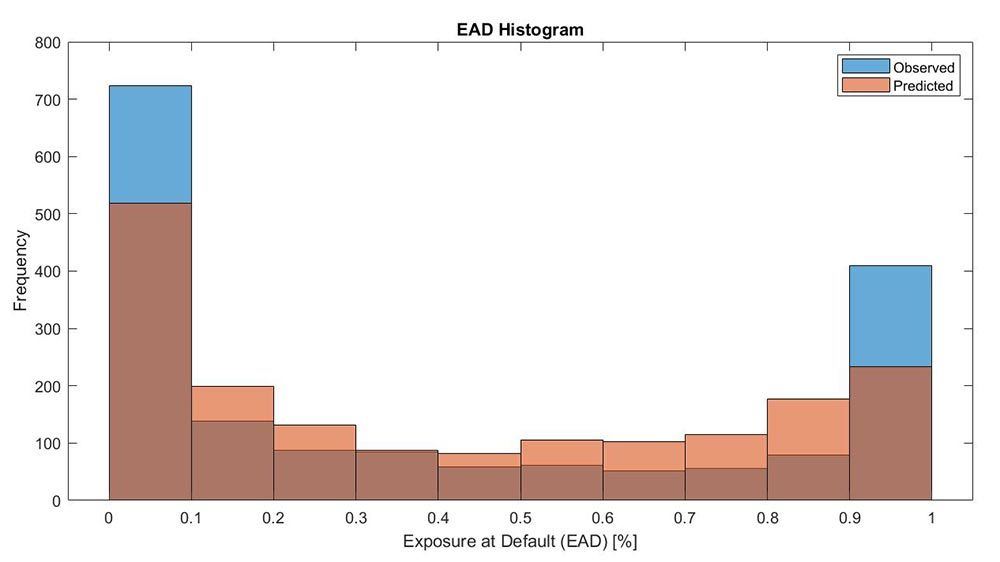

Exposure at Default (EAD) Models

Predict the loss exposure for a creditor when a debtor defaults on a loan using regression and Tobit models.

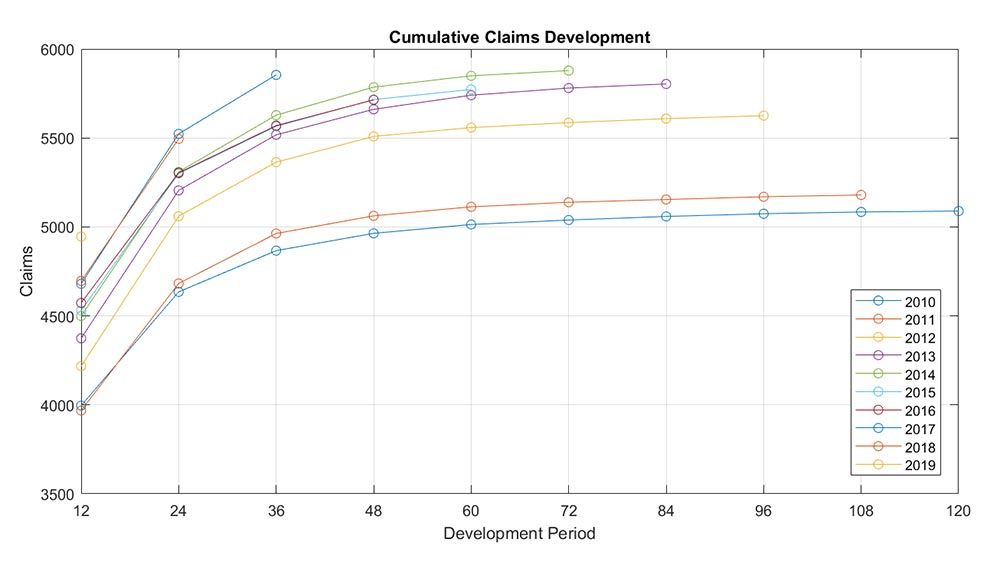

Insurance Risk Modeling

Calculate the risk of loss from mortality and unpaid claims, and estimate ultimate claims using the chain ladder bootstrap method.